Ontario represents a unique anomaly in North American iGaming. Since its transition to a fully regulated, open-license model in April 2022 under the purview of the Alcohol and Gaming Commission of Ontario (AGCO) and iGaming Ontario (iGO), the province has matured at an aggressive pace.

As of early 2026, the initial “land grab” phase has ended. Operators have shifted their focus from sheer market share acquisition to optimizing unit economics—specifically focusing on Customer Acquisition Cost (CAC), Lifetime Value (LTV), and player retention. Here is an analysis of the current customer and operator behaviors in Ontario, benchmarked against mature US markets.

- Customer Behavior: Spend, Frequency, and Yield

The Ontarian player base has proven to be highly lucrative and deeply engaged, driven predominantly by the online casino sector.

- Unprecedented Wager Volumes: In the 2024–2025 fiscal year, Ontario recorded C$82.7 billion in total wagers, generating C$2.9 billion in total gaming revenue—a massive 30% year-over-year increase.

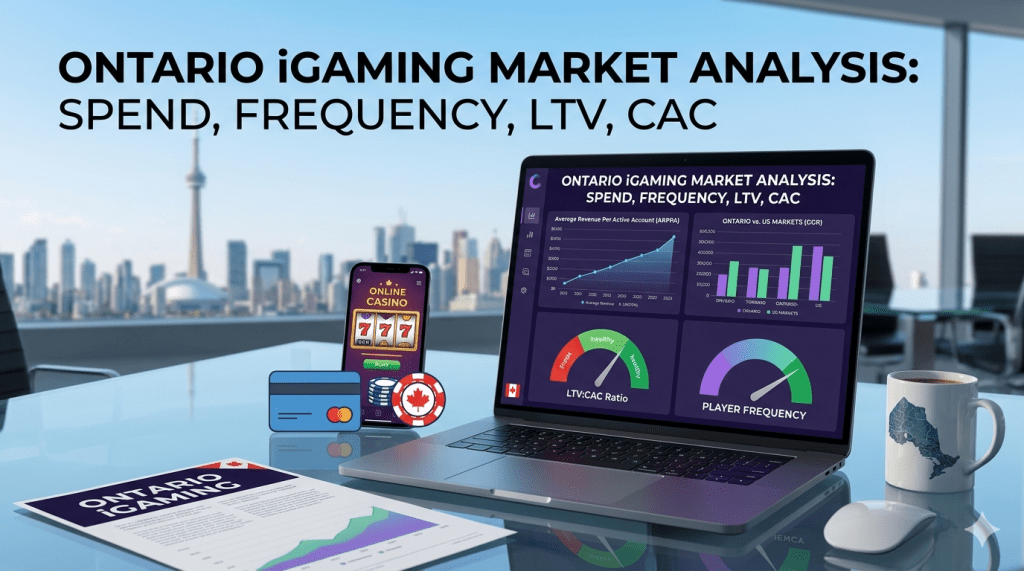

- ARPPA (Average Revenue Per Active Account): Player yield has steadily climbed. As of late 2025, the monthly ARPPA reached C$334, representing a 13% annual growth. This points to a maturing player base that is depositing more frequently and consolidating their play with fewer, preferred operators.

- The Casino Dominance: Unlike early US markets where sports betting was the primary acquisition engine, Ontario is overwhelmingly casino-first. Online casino products account for roughly 87% of all wagers and over 75% of net gaming revenue.

- Product Shifts: We are observing a significant consumer shift toward Live Dealer games and high-volatility slots. Live Dealer bridges the trust gap for legacy land-based players, increasing average session lengths and overall frequency.

Analyst Note: The rising ARPPA paired with a stabilizing number of active accounts (around 1.27 million monthly actives) indicates a classic market maturation. The growth is no longer coming from new players, but from the increased monetization and retention of existing players.

- Operator Behavior: The LTV vs. CAC Squeeze

Ontario’s regulatory framework dictates a vastly different operational playbook compared to the US, fundamentally altering unit economics.

The Marketing Restriction (The CAC Driver)

Under AGCO regulations, operators are strictly prohibited from publicly advertising induction bonuses (e.g., “Deposit $10, Get $100”). Bonuses can only be offered directly on the operator’s platform or through explicit opt-in communications.

- Impact on CAC: Without the easy bait of public free bets, operators rely heavily on brand-building, sports team sponsorships, and high-cost affiliate networks. Consequently, blended CAC in Ontario is higher than the early days of US markets. For standard players, CAC hovers between C250–C400, while VIP/High-Roller CAC can easily stretch between C500–C850.

KYC Friction and Drop-offs

Ontario enforces strict, front-loaded Know Your Customer (KYC) and Anti-Money Laundering (AML) checks, alongside enhanced responsible gaming triggers. Operators who delay KYC until a player’s first withdrawal face massive compliance risks, but those who enforce it at sign-up see top-of-funnel friction. Top-tier operators have invested heavily in automated identity verification APIs to streamline onboarding, directly reducing CAC by improving the click-to-deposit conversion rate.

The Focus on LTV

Because top-of-funnel acquisition is expensive and restricted, operators are forced to prioritize LTV.- Target Ratios: A healthy iGaming operation in Ontario is currently targeting a post-bonus LTV:CAC ratio of at least 1.5x to 2x within the first 12 months.

- Retention Tools: Operators are heavily utilizing AI-driven CRM tools for hyper-personalized bonusing, predictive churn modeling, and omnichannel loyalty programs to keep the C$334/month player from migrating to a competitor.

Benchmarking: Ontario vs. Mature US Markets

To truly understand Ontario’s trajectory, it must be benchmarked against the “Big 3” US iGaming states: Michigan, New Jersey, and Pennsylvania.Metric / Market CharacteristicOntario (Canada)Michigan (US)New Jersey (US)Launch DateApril 2022January 2021November 20132025 Gross Receipts / GGR~C$2.9 Billion (~$2.1B USD)~$3.8 Billion USD>$3.5 Billion USDDominant Revenue DriverOnline Casino (75%+)Online CasinoOnline CasinoPublic Bonus AdvertisingStrictly ProhibitedPermittedPermittedTax Rate~20% (Revenue Share)20% – 28% (Tiered)15%Market ConcentrationHigh fragmentation (50+ active operators)Top-heavy (DraftKings, FanDuel, BetMGM dominate)Top-heavyKey Comparative Insights:

- Cross-Sell Efficiency: Michigan boasts some of the highest cross-sell rates from sports to casino in North America. Ontario operators are mirroring this strategy, using the lower-margin sports betting product as an acquisition funnel to port players into the high-margin online casino ecosystem.

- Market Fragmentation: Because of the relatively accessible 20% tax rate and open licensing model, Ontario supports over 50 licensed operators. In contrast, Michigan and New Jersey are heavily consolidated around the top three or four US brands. For investors, this fragmentation in Ontario signals upcoming M&A activity, as mid-tier operators with high CACs will inevitably be absorbed by larger players seeking to acquire player databases.

- Growth Trajectory: While Michigan hit a staggering $3.8 billion USD in total gross receipts in 2025, Ontario’s 30% YoY growth suggests it is rapidly closing the gap, driven by a slightly larger population base (approx. 15 million in ON vs. 10 million in MI) and a deep-rooted cultural affinity for casino gaming.

Strategic Takeaways for Investors- Look Beyond Handle: Gross wager volume is a vanity metric in Ontario. Analysts should scrutinize operator Net Gaming Revenue (NAGGR) to Wager margins. Operators efficiently managing their promotional spend and mix of high-margin products (like slots and live dealer) will present the best return profiles.

- Technology is the Moat: Operators possessing proprietary tech stacks for seamless KYC onboarding and localized payment processing (e.g., Interac integration) hold a definitive advantage in lowering CAC.

- M&A is Imminent: The Ontario market cannot sustain 50+ operators under current CAC conditions. Expect well-capitalized market leaders to acquire smaller, niche operators simply to buy their active player databases and bypass the expensive top-of-funnel acquisition process.

Leave a comment