When we underwrite an OSB operator, the first structural question is not market share or brand. It is: who owns the technology?

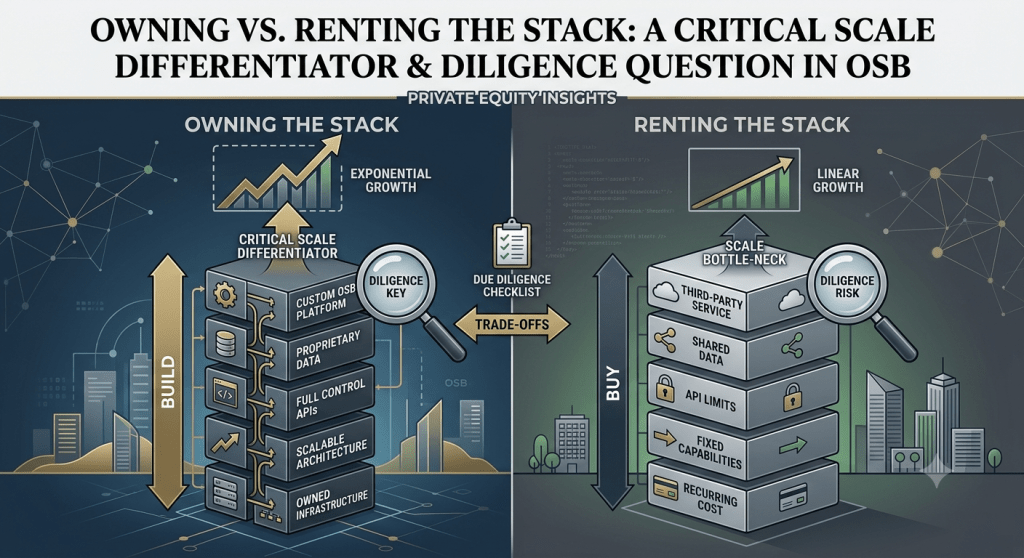

The U.S. market is roughly split between operators running on a proprietary, vertically integrated platform and operators running on a licensed third-party platform. The distinction looks academic until you model it. A licensed platform typically carries a revenue-share or per-bet fee that scales directly with handle — meaning the operator’s cost of goods sold rises in lockstep with its success. The vertically integrated operator converts that same growth into operating leverage.

Owning the stack also controls the product roadmap. The operators that shipped micro-markets, live cash-out, and novel parlay constructs first were, almost without exception, the ones who didn’t have to wait in a supplier’s development queue. In a market where product velocity drives engagement and engagement drives hold, controlling your own roadmap is a compounding advantage.

The counterargument is capital intensity: building and maintaining a trading platform costs hundreds of millions of dollars and years of effort. For a subscale operator, renting is the only rational choice. That is precisely why we believe the mid-tier of the U.S. market is structurally unstable — too big to rent economically, too small to build. That tension, in our view, is what drives the next wave of consolidation.

Leave a comment