For more than a decade, bet365 was the operator everyone in US sports betting talked about but couldn’t actually use. Founded in 2000 by Denise Coates in Stoke-on-Trent, England, it grew into one of the world’s largest online gambling companies on the strength of a deep in-play product, live streaming, and a fiercely private, founder-controlled ownership structure.

In the US it arrived late and moved deliberately. By mid-2026 it had become one of the more interesting strategic stories in the market: a privately held challenger spending aggressively to buy share while the rest of the field pulled back. This is a profile of that business — its financials, its enterprise value, its state footprint, its product, and the marketing posture that sets it apart.

A profit squeeze driven by expansion

Bet365 Group remains privately owned and headquartered in Stoke-on-Trent, controlled by the Coates family. Denise Coates is founder and co-CEO alongside her brother John; she holds roughly a 58% stake. That ownership matters for the US strategy, because it frees the company from the quarterly earnings pressure DraftKings and Flutter (FanDuel) face.

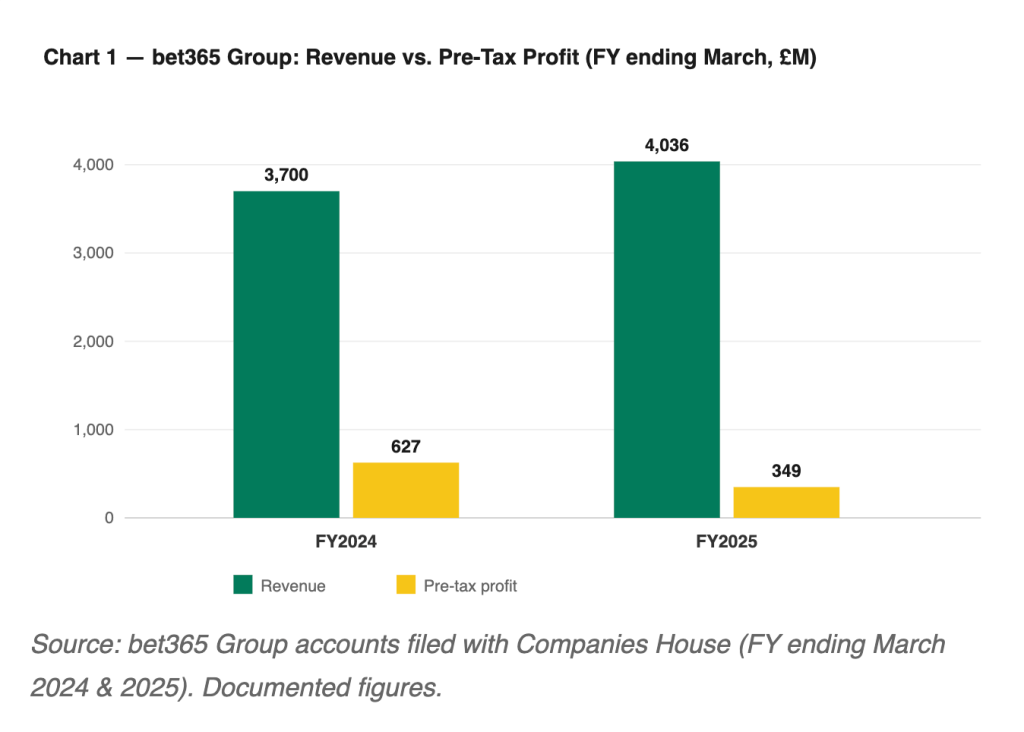

The most recent published accounts, for the fiscal year ended March 30, 2025, tell a story of top-line growth bought at the cost of profitability. Revenue rose roughly 9% to about £4.04 billion (~$5.45 billion), driven by a ~5% increase in sports and a ~25% jump in gaming. But pre-tax profit fell about 44%, to roughly £348.7 million from £627 million the prior year, and direct costs ballooned from about £686.8 million to about £896.5 million, including a one-off ~£59.2 million restructuring charge. Revenue up, profit sharply down:

Management has been explicit that the compression is a function of new-market entry costs — launching in regulated US states and in Brazil, Peru, and Serbia carries heavy upfront marketing, tax, and compliance loads. During the same period bet365 exited China, historically one of its largest grey markets, signaling a pivot toward regulated jurisdictions on both sides of the Atlantic. Despite the profit slide, Denise Coates again drew one of Britain’s largest pay-and-dividend packages, reported in the £260m–£287m range for the year. And in spring 2025, reports emerged that the family had spoken with Wall Street advisers about a full or partial sale — the China exit widely read as housekeeping to simplify diligence.

Enterprise value

Bet365 is private, so there is no market cap — only deal chatter and analyst estimates. When sale talks surfaced in spring 2025, the figure attached was around £9 billion (~$12 billion at the time). Eilers & Krejcik Gaming (EKG) independently valued the group at up to ~$12 billion, anchored on the prior year’s £627 million pre-tax profit. Several advisers argued that looked light versus listed peers — DraftKings’ public market cap sat near $16–17 billion at the time on a US-only footprint. Sell-side estimates for the group have spanned roughly $9 billion to $16 billion.

US revenue share: a small base growing fast

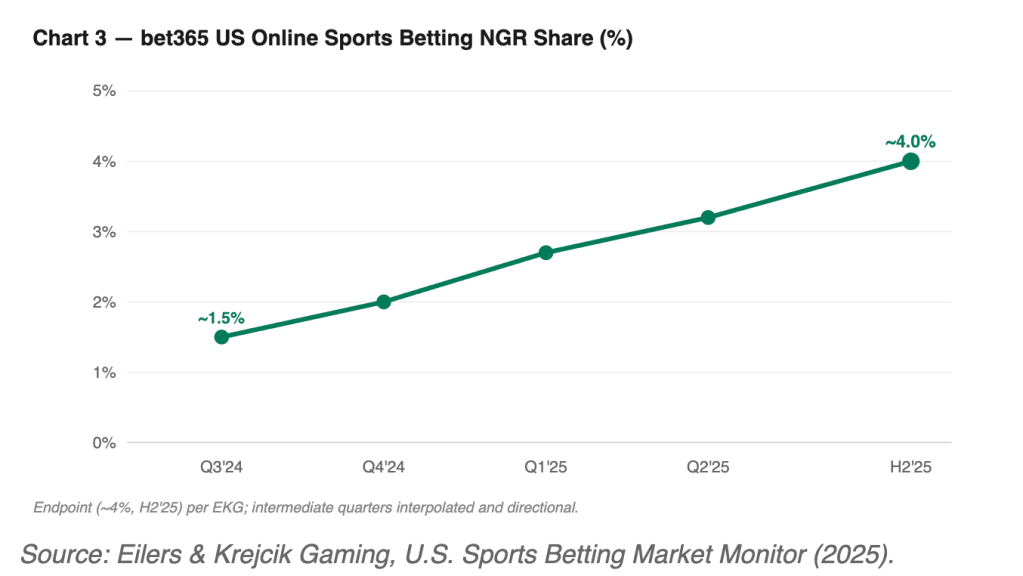

By the second half of 2025, bet365’s nationwide US online sports betting net-revenue (NGR) share had reached roughly 4%, with EKG calling it the operator’s best US quarter yet. That places it well behind the FanDuel/DraftKings duopoly but firmly in the chasing pack alongside BetMGM, ESPN Bet, and Fanatics. The rise has been driven primarily by stacking new state launches — growing by being in more places, not yet by out-competing the leaders head to head.

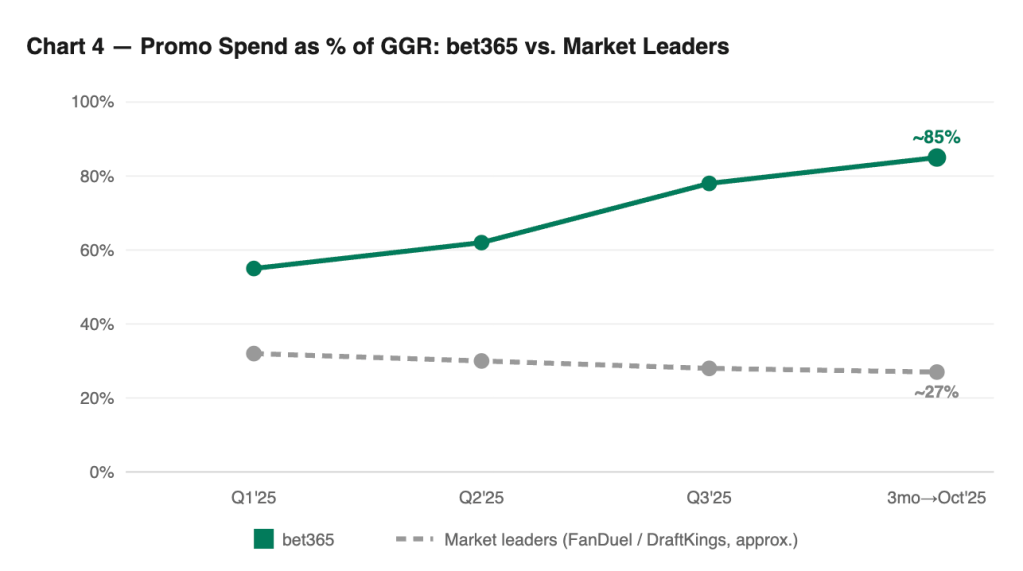

The signature trend: counter-cyclical promo spend

The most distinctive feature of bet365’s US business is how it pays for that growth. While promotional spend across the industry — including FanDuel and DraftKings — has been flat to declining since the start of 2024, bet365 went the other way. EKG data showed its promo spend in the three months ending October 2025 approached 85% of gross gaming revenue — by a wide margin the highest ratio of any US operator. This is the mechanical twin of Chart 1: the group profit squeeze and the US promo burn are two views of the same strategy.

State access: 16–17 states and counting

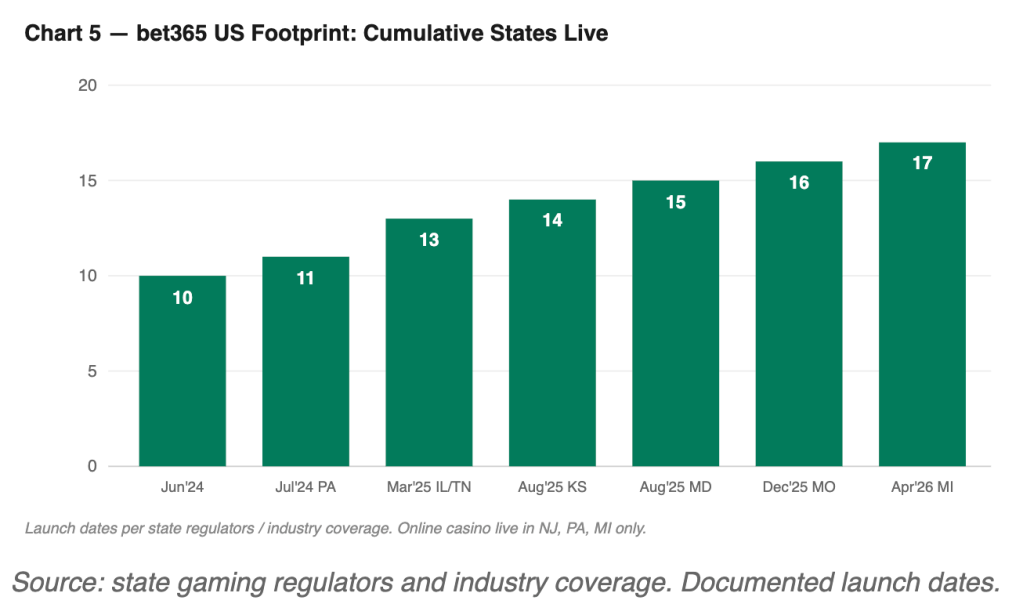

Bet365 entered later than the first wave and has climbed the ladder steadily. As of mid-2026 it is live in roughly 16–17 states, depending on the date and whether the most recent launch (Michigan, April 2026) is counted. The footprint spans Arizona, Colorado, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maryland, Missouri, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, and Virginia, plus Michigan.

Because most states require attaching to a land-based license holder, expansion has been built on market-access deals — the Ak-Chin Indian Community in Arizona, Hard Rock Atlantic City in New Jersey, Presque Isle Downs in Pennsylvania. Two structural points stand out. First, bet365 is conspicuously absent from the largest betting populations — New York (it holds only a retail position at Resorts World Catskills), California, Florida (closed by the Seminole Tribe’s exclusivity), and Texas (no legal online betting). That caps its near-term addressable market regardless of execution. Second, its online casino footprint is far narrower than its sportsbook — live in only New Jersey, Pennsylvania, and Michigan. Since iGaming is materially more profitable than sportsbook, limited casino access constrains the blended economics of the US business.

Product: the in-play DNA

If marketing spend is bet365’s most distinctive financial trait, product depth is its most distinctive competitive one. The global reputation was built on live, in-play betting, and that DNA carries straight into the US app.

In-play and live streaming. bet365 runs what is widely regarded as the largest in-app live-streaming library of any US-licensed book — frequently cited at more than 70,000 events streamed annually in the US (and north of 750,000 globally), at no extra subscription cost; access typically requires a funded account or a bet in the prior 24 hours. The streaming is tightly integrated with live markets, creating a watch-and-bet experience few US rivals match, with latency reviewers peg around 15–20 seconds. The live menu is deep, spanning quarter-by-quarter markets, player props, and niche sports like cricket, rugby, and snooker that most US books underweight.

Bet Builder and Same Game Parlay. The SGP product runs through bet365’s Bet Builder, with Bet Builders+ / SGP+ letting users combine SGPs from different games into a single multi-game ticket — its answer to the cross-game SGP products that have become the industry’s profit engine. An in-play Bet Builder allows construction during a game.

Cash Out and Edit Bet. An early pioneer of Cash Out, bet365 offers a granular version: Partial Cash Out (settle part, let the rest ride — up to ~10 times on straights, 5 on parlays) and Auto Cash Out (preset a target). Its Edit Bet feature — add, swap, or remove selections on an unsettled bet, including in-play — remains rare among US books and is a genuine differentiator.

Promo mechanics. Bet Boost (a daily, bookmaker-priced list of enhanced multi-leg single-event parlays — the counterpart to FanDuel’s SGP Boost and DraftKings’ Profit Boost, but priced by bet365); escalating parlay/ACCA bonuses scaling from a small percentage on two legs up to as much as 100% on long-shot tickets; and Early Payout, which settles certain bets as winners once a team builds a defined lead. The cumulative effect is a product built for engaged, in-play bettors rather than purely casual parlay players.

Marketing: “Never Ordinary” and a counter-cyclical bet

bet365’s brand platform is “It’s Never Ordinary,” launched in 2023 and extended with blockbuster “Breaking News” creative — sporting-spectacle ads built around a fictional sports news channel covering absurd, extraordinary moments. The work deliberately foregrounds the live, in-play world that is the product’s core, and runs across multiple territories including the US.

Three things separate its approach from US-native rivals. It is product-led — selling the in-play and streaming experience rather than leaning primarily on welcome-offer dollar figures. It has global sponsorship muscle a US-only operator can’t replicate, becoming the first sports betting brand to sponsor the UEFA Champions League and adding partnerships such as the UFC. And it runs a counter-cyclical spending posture, pushing promo to industry-leading levels precisely while rivals retrench (Chart 4), launching its first dedicated North American campaign, and exiting the American Gaming Association to chart an independent path. Welcome offers — a “bet $5, get bonus bets” promo, a larger first-bet safety net in states like New Jersey and Colorado — are tuned state by state. The through-line is patience funded by private ownership.

The bottom line

bet365’s US business is best understood as a deliberate, well-capitalized land grab by an operator that can afford to be patient. The cost shows plainly: group profit down sharply (Chart 1) while US promo spend sits at the top of the industry (Chart 4), and a US revenue share around 4% (Chart 3) built mostly by adding states (Chart 5) rather than winning head to head. On valuation, the group is worth on the order of $12 billion, but the US is a minority slice — perhaps 10–20%, and that slice is an option on the future rather than a reflection of present cash (Chart 2). The footprint remains locked out of the biggest prizes and thin on high-margin iGaming. The product is arguably best-in-class for engaged bettors, and the marketing sells that product rather than just a sign-up bonus.

Whether it pays off depends on two things bet365 only partly controls: how many more — and how large — the states it can enter become, and how long the Coates family’s private patience (or a sale or listing) sustains the spend. For now, the sleeping giant is starting to show signs of making more noise.

Leave a comment